Loan consolidation is a very popular service. How to choose the most suitable offer and what you need to pay attention to, read in our material.

Today, a lot of people deal with loans. At the same time, most borrowers pay more than one debt. And each has its term, amount, bank, where to take the money. It is clear that this is not entirely convenient – and if there are more than two loans, this turns into a problem.

Statistics: According to Bankrate’s study, which analyzed the responses of more than 160,000 applicants, debt consolidation was the most commonly mentioned reason for obtaining a loan in the first quarter of 2020 – 38%.

Today, many organizations offer to combine loans — take a new loan, under more favorable conditions, and pay only for it. When is it worth doing, and when is it not?

(Source: Experian)

Pros to Use Debt Consolidation

Consolidation combines several credit accounts into one to pay the debt. As a rule, a reduced rate is applied to such debts. A single account is also convenient for other reasons:

- it is easier to manage;

- the debt repayment scheme is developed for a particular client, depending on his material situation;

- co-borrowers, collateral, and guarantors of the transaction can be involved;

- credit rating is increased as the number of regular payments is reduced;

- the total amount of monthly payments is reduced;

- less is spent on fees for servicing several bank accounts, transactions;

- service in one financial institution;

- with successful completion of the program, the credit history improves.

Financial managers and consultants are usually involved in the preparation of a debt consolidation program. After meeting with their client, they find out the reason for the failure to repay the loan, and then determine under what conditions their client is able to repay it. Refinancing may be an option for borrowers who have difficulty repaying their loans, however. For student loans, there is an alternative loan available from a private lender with more favorable terms than the existing loan. You must perform thorough research, compare numerous options, and choose the best company to refinance your student loan.

An additional advantage will be that you can consult not only on credit issues, but also receive, for example, financial assistance for medical bills, installment loans review from Fit My Money, budget management, long-term income and expenditure planning, and more.

How many loans can you consolidate?

Usually from practice from five to seven inclusive. Although some programs do not limit the number of such “debts” to unification.

Which loans can be combined?

Various: commodity, consumer, automobile, and others. Difficulties can arise with loans that you took in foreign currency – not everyone takes to work with them.

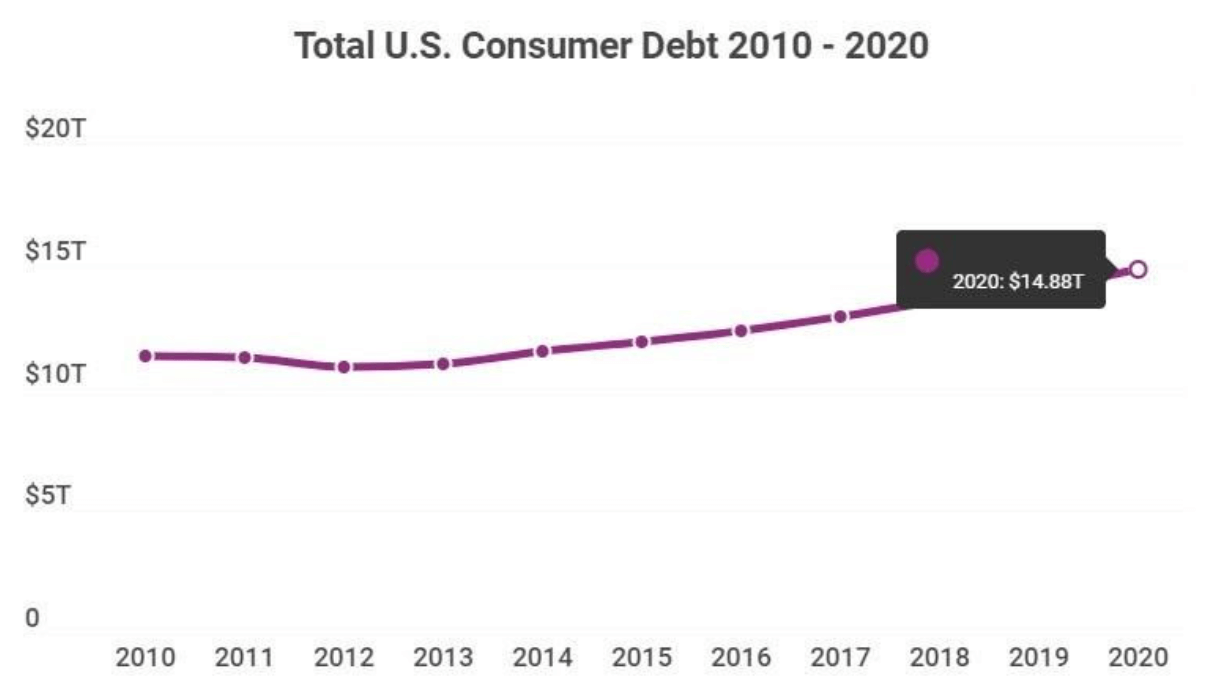

Statistics: Student loan debt saw the largest growth (12%), followed by mortgage debt (7%) and personal loan debt (6%), according to Experian data from Q3 2020.

Deficiencies in Loan Pooling

You can use such a program only for good reasons – for example, due to illness or dismissal due to a reduction in staff. This is especially true for secured loans. After all, banks are more willing to go to the procedure of forced collection of debt:

- more often offer the program to selected clients;

- the borrower must be solvent;

- the consolidation service is paid;

- the lender requires collateral or surety;

- with poor payment discipline, stricter conditions are introduced;

- not all banks have such a service.

Tips and Recommendations

When borrowing money from a bank through credit cards or personal loans, it is sometimes impossible to pay them back because there are high-interest rates or unforeseen financial expenses that will never get rid of debts. Debt consolidation can help pay off debts much faster while making small monthly payments to only one lender.

A few tips to follow if you chose debt consolidation:

- Choose a consolidation of credit debt, and see what monthly payments were previously paid, this reduces the risk of spending money for the wrong purpose and faster to pay it off.

- Do not issue new credit cards and other loans for at least 6 months after completing debt consolidation.

- Try to pay more than the minimum monthly payment to reduce your debt as quickly as possible.

- Do not miss a single payment on the consolidation loan, this may negatively affect the credit report, and the interest rate will increase.

- Ensure that the credit report does not contain errors or omissions before submitting your application.

- Learn about any subscription fee for debt consolidation, since most banks hide this information and indicate it in small print or in the form of an addition to the loan agreement.

Experts recommend not to submit an application immediately. First, it is better to evaluate all your loans and repay the most insignificant. This will not only reduce the burden but also improve the reputation, increase the chances of a positive bank response.

It is not recommended to agree to a secured loan if unsecured loans are involved. If the client does not comply with the terms of the agreement or the payment schedule, he may lose valuable property. The duration of the contract is important: the longer it is, the greater the overpayment will be. You will also have to repay the loan on the card, even if the grace interest-free period has not expired.